Growing Credit Card Spends Through Deeper Customer Engagement : Trends and Strategies for 2026

It’s January 2026. Banks are deep in annual planning cycles, reviewing what worked last year and sketching out targets for this one. What’s evident is that the landscape is undergoing a fundamental shift with two sets of credit card issuers. The ones that are still relying on static campaigns and SQL-based data queries and at the other end, forward-thinking card issuers that are racing ahead with hyper-personalized experiences, dynamic multi-currency rewards, and AI-driven engagement engines. The gap between innovation leaders and laggards is widening, and it’s driven by one critical insight: the era of one-size-fits-all credit card engagement is over.

A leading banking partner deployed this shift and, within 12 months, built 150+ campaigns across their lifecycle, achieved 23%+ spend increases on milestone offers, and converted 17% of dormant accounts. The numbers tell a story: when you change how you engage, the results follow.

If your annual plan still mirrors last year’s playbook, this is worth reconsidering.

The Four Shifts That Matter

From Generic Campaigns to Personalized Experiences

The traditional credit card playbook relied on mass campaigns. The same promotional message sent to large customer cohorts using static demographic filters. The result : baseline engagement, high acquisition costs, revenue left on the table.

The structural problem is that legacy systems built on SQL databases and batch processing force banks to think in segments rather than individuals. A customer with three years of transaction history is treated identically to someone who just received their card.

Today’s approach is different. Banks are deploying real-time cohort creation and intelligent nudging, where every interaction is informed by actual behavior. A customer who regularly spends on fuel but has gone dormant receives a contextual nudge tied to their spending patterns, not a generic message. A customer inching toward their annual fee waiver gets an offer that bridges that specific gap.

This works because hyper-personalization is measurable in the form of meaningful lifts in activation, spend, and portfolio returns.

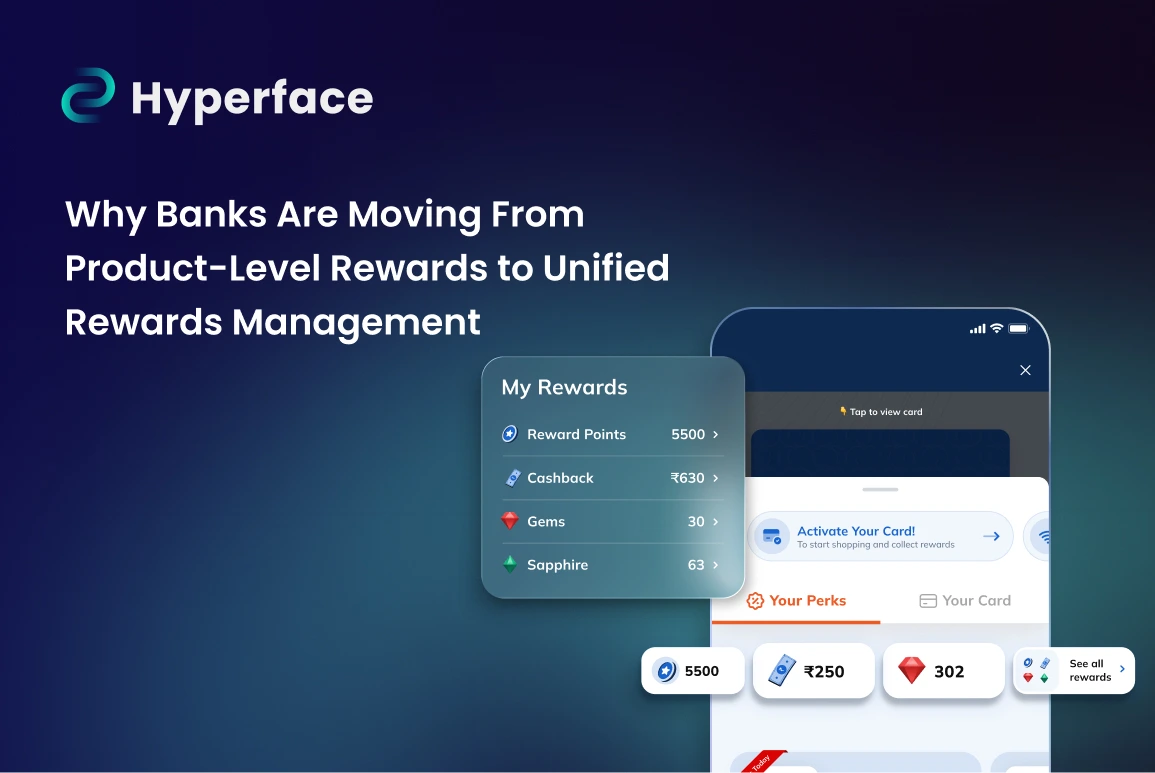

From Static Rewards to Dynamic, Multi-Currency Ecosystems

Static rewards programs feature flat cashback layers, fixed redemption rates and limited choices.

But customer expectations have shifted. Cardholders now want rewards that match their actual spending and lifestyle.

The sophistication required here is twofold: real-time reward computation and ecosystem integration. Modern platforms now adjust reward tiers based on customer cohorts, spending velocity, and business goals. Rewards update in real-time, get tested across variants, and optimize for conversion without operational strain.

The move toward multi-currency rewards and interoperable ecosystems means banks can offer genuine value beyond merchants. Think pay-by-points and instant, multiple on-ground redemption opportunities.

From Data Fragmentation to a Single Source of Truth

This is perhaps the biggest issue. Legacy banking stacks fracture customer data across systems: core banking, payments, CRM, partner integrations, marketing automation. Launching a campaign requires extracting data from multiple places, manually reconciling conflicts, and moving forward with inevitable lag.

As a result, opportunities that need to be seized immediately, say, a customer becoming eligible for a credit limit increase or a transactional milestone achieved, get missed because the data isn’t unified.

Modern platforms center on unified customer data that feeds into a powerful orchestration layer. This layer ingests account data, transactions, and behavioral signals in real-time, enabling banks to:

- Build cohorts dynamically (e.g., “customers with declining fuel spend, active at automobile retailers”)

- Trigger campaigns instantly when conditions are met

- Track performance with granularity (conversion rates by variant, spend lift by cohort)

- Iterate quickly without waiting for IT cycles

A leading bank that deployed this approach built 150+ campaigns across customer lifecycle stages (acquisition, activation, expansion, reactivation, upsell) in under 12 months. That scale isn’t possible with fragmented systems.

From Superficial Gamification to Purposeful Engagement Design

The science is clear: gamification in banking when designed thoughtfully is a genuine driver of behavior change.

Effective gamification in credit card programs ties to real outcomes: milestone achievements, spending goals, rewards redemption. Progressive milestones work because they create momentum. A customer isn’t just spending; they’re progressing toward outcomes. Real-time progress tracking (“4 transactions to go” or “spend more to unlock”) creates psychological pull. Contextual nudges at critical moments (when a customer is 75% of the way) drive conversions.

In practice, banks using this approach see material uplifts. One program achieved 23%+ spend increase from their festive spend uplift campaign by incorporating gamification. Another saw 46.3% higher spend from targeted nudges in low-activity segments.

Why These Gaps Are Hard to Fix

The tricky part isn’t intent but the infrastructure to achieve it. You can’t personalize in real-time when customer data lives in six different places. You can’t offer dynamic rewards when your rewards engine updates quarterly. You can’t create engaging experiences when your engagement platform sits on top of systems that weren’t designed for any of this.

What you need is a layer that connects everything and makes modern engagement actually possible. One source of truth. All customer data in one place, updated in real-time, accessible to every system that needs it. Real personalization that understands where each customer is in their journey and responds accordingly. Flexible rewards: multi-currency frameworks, points, cashback, partner currencies, all in one system. And everything is connected, so every touchpoint has context.

That’s what Smart Engage was built to solve.

What Real Engagement Should Look Like

Rather than treating engagement as a marketing afterthought, Smart Engage is a unified orchestration layer purpose-built for credit card lifecycle management. It layers on top of the existing bank stack. You’re not ripping anything out. You’re making it all work together in ways it couldn’t before.

Here’s what sets it apart:

Automated Portfolio Management: A single dashboard consolidates partner integrations, customer experiences, campaign configurations, and analytics. Banks build, run, and scale campaigns without coordinating across multiple teams and systems. The platform automatically handles data ingestion, cohort management, and benefits processing.

Real-Time Personalization: Smart TagsTM enable dynamic cohort management. Instead of monthly batch processes, cohorts update in real-time based on behavior. A bank can define: “Customers with declining fuel spend who are active at automobile stores” and campaigns automatically target that cohort as it evolves.

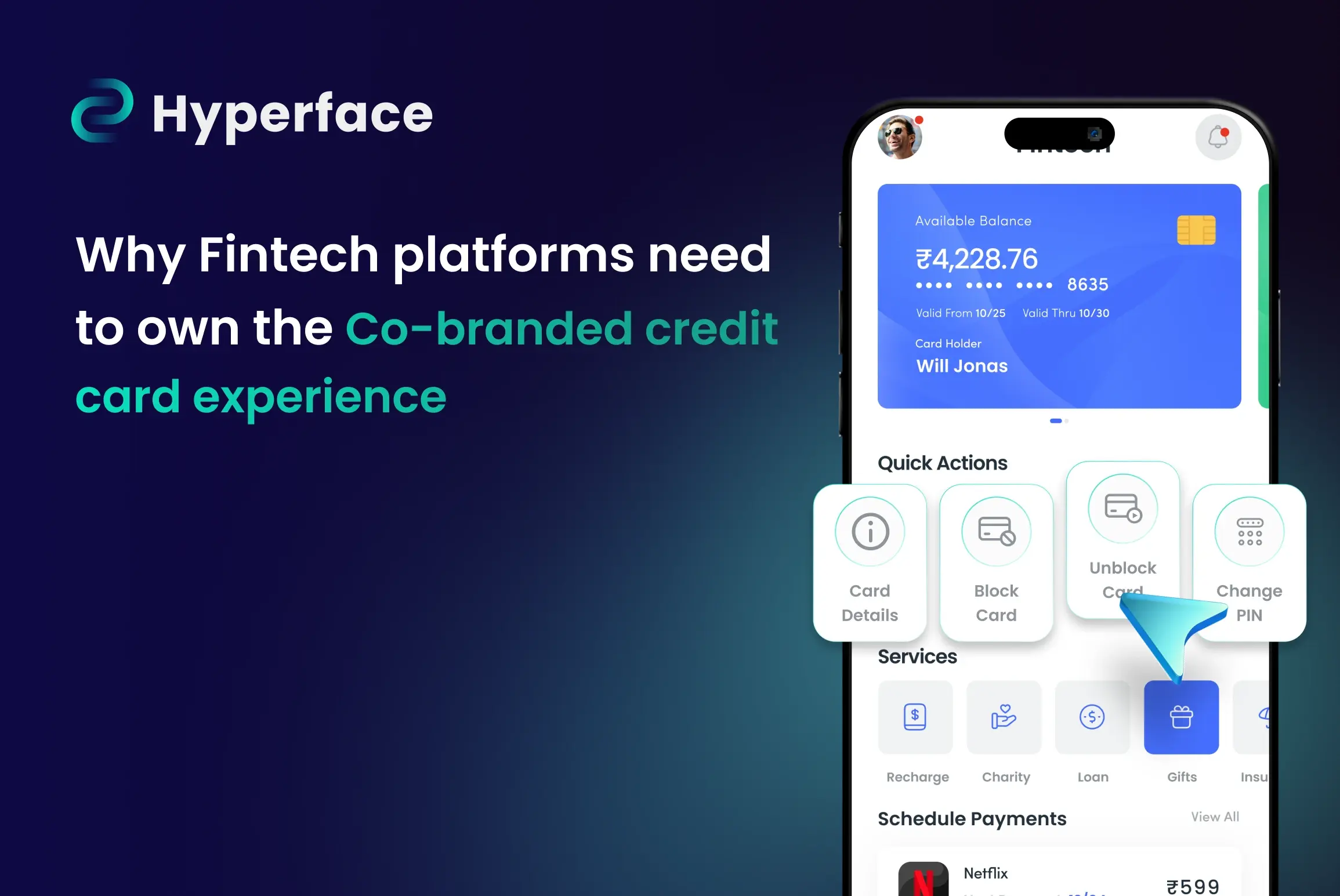

Contextual Nudging: Smart Nudges deliver timely, relevant messages informed by customer eligibility, transaction history, and campaign context. A customer receives an EMI conversion nudge after a large purchase (when the need is real) rather than randomly. A customer nearing a milestone gets progress updates with their exact standing.

Automated Reward Computation: Reward rules are defined once. The system handles real-time calculations, accruals, and redemptions. This matters for complex structures: bonus points during specific windows, category multipliers, milestone-based benefits.

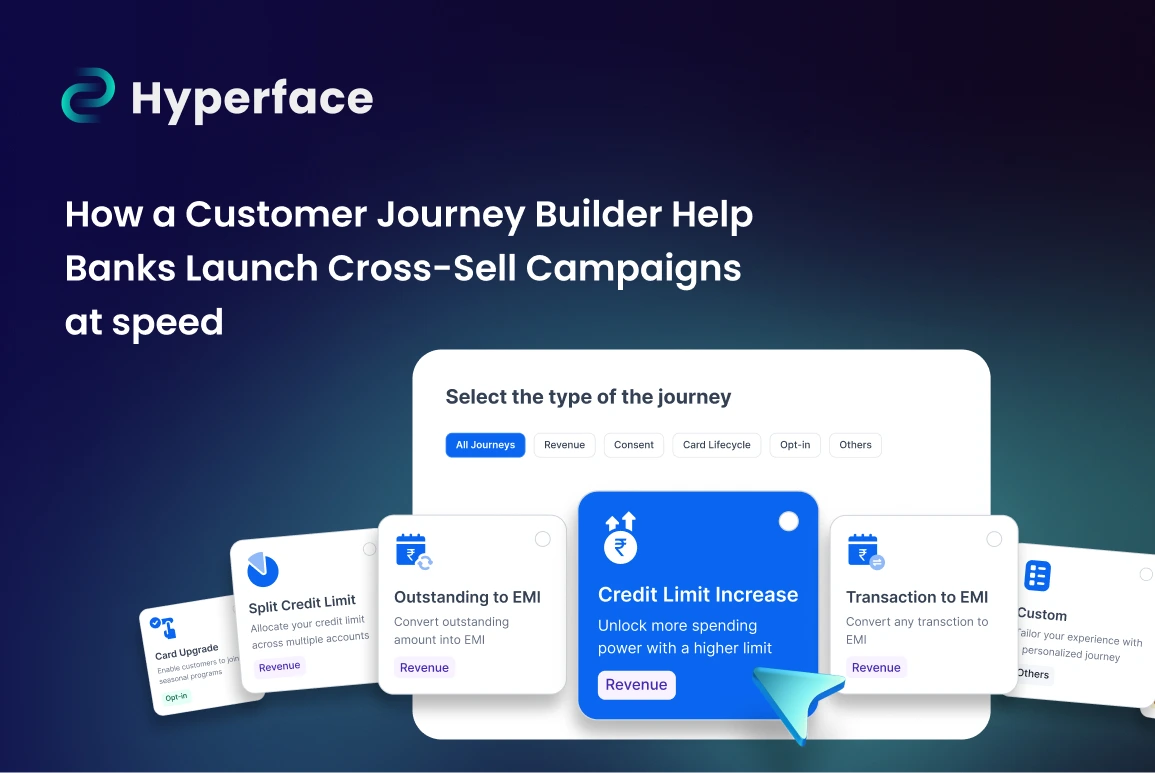

Pre-Built Journey Templates: Common business use cases like EMI conversions, credit limit increases, dormant reactivation, and seasonal campaigns launch faster. The platform is also extensible: banks design custom journeys for unique needs with minimal development work.

Compliance-First Architecture: As regulatory guidelines constantly evolve, Smart Engage includes audit trails, maker-checker controls, and transparent logic, ensuring banks stay compliant even as they innovate.

Real-World Impact: What the Numbers Show

A leading bank deployed Smart Engage and, within 12 months, achieved:

- 150+ campaigns across the customer lifecycle

- 23%+ spend increase from milestone campaigns

- 46.3% higher spend from nudges to inactive customers

- 17% conversion from dormant account reactivation

- 10+ campaigns running daily, with personalized credit card engagement and data-driven

These outcomes reflect the compound effect of better data, real-time personalization, and thoughtful engagement design.

The 2026 Imperative: Move Now or Fall Further Behind

The credit card market is throwing up two distinct groups of issuers. Banks that iterate quickly, personalize meaningfully, and measure rigorously, are pulling ahead. Those relying on generic campaigns and legacy systems are losing ground.

The barrier isn’t capability. Modern technology is now API-driven, plug-and-play, fast to implement. The barrier is speed of execution.

Customer expectations have shifted fundamentally. Personalization isn’t a luxury; it’s expected. Banks winning this year are deploying modern platforms, learning from data in real-time, and building loyalty through relevance.

Are you a bank looking for a credit card engagement playbook that delivers real ROI? Chat with us today to learn more about our implementations and use cases.

About Smart Engage: Smart Engage powers personalized credit card engagement for leading banks, enabling them to build and scale innovative programs with real-time personalization, unified data, and compliance-first architecture. Learn more at hyperface.co