How a Customer Journey Builder Help Banks Launch Cross-Sell Campaigns at speed

In brief

- Cross-sell and up-sell are taking on a larger share of the credit card P&L as revolving income growth moderates and banks become more selective about new customer acquisition.

- The principal constraint on campaign launch speed in retail banking is structural: customer journeys are tightly coupled to the native mobile app.

- A no-code journey builder decouples revenue journeys from the app and distributes them through WhatsApp, SMS, and email, compressing launch cycles from months to days.

- The shift relocates journey orchestration from an engineering dependency to a marketing-led capability.

________________________________________________

As revolving income growth moderates and banks become more selective about new customer acquisition, cross-sell and up-sell are taking on a larger share of the credit card P&L: EMI conversion, credit limit increases, card upgrades, and cross-sell to allied banking products. The time required to design, approve, and launch a single campaign, however, often remains considerable. In this article, read about how no-code customer journey builders address that gap and enable banks to launch revenue campaigns at speed.

Why Bank Revenue Campaigns Face Systemic Launch Delays

Across most retail banks, customer journeys remain tightly coupled to the mobile app. That coupling introduces three recurring sources of delay.

Release cadence. In-app changes are subject to App Store and Play Store review cycles, monthly release trains, and code-freeze windows aligned to regulatory reporting calendars. Configuration-level changes inherit the same cadence as full feature releases.

Cross-functional approval chains. Even routine journey changes can require sequential sign-off across risk, legal, compliance, and product. End-to-end approval adds materially to launch timelines.

Limited experimentation surface. Because each variant requires a release, teams have constrained capacity to A/B test, iterate on creative, or respond to live behavioral signals between release windows.

The cumulative effect is a measurable gap between strategy and go-live.

What Is a Customer Journey Builder?

A customer journey builder is a no-code or low-code platform that allows bank product, marketing, portfolio and growth teams to design, launch, and measure end-to-end customer flows — onboarding, EMI conversion, credit limit increase, consent collection — without writing app code or waiting for the next release cycle.

The defining characteristics:

Decoupled from the native app. Journeys are hosted as standalone, browser-based experiences outside the bank’s mobile application.

Distributed through high-conversion channels. Each journey is delivered via a unique, customer-specific link sent over the bank’s owned channels – WhatsApp, SMS, email, or push.

Driven by smart targeting. Journeys reach the right customer at the right moment, using behavioral tags and event-based nudges.

Measured in real time. Conversion analytics return instantly, allowing teams to adjust copy, offers, and flow logic mid-campaign.

How Hyperface Journey Engine Addresses Operational Bottlenecks

Hyperface Journey Engine is a plug-and-play journey orchestration platform built for banks. It operates alongside the bank’s core systems and mobile application, delivering personalized journeys to the customer through the channels they already use.

The platform operates across three capabilities.

1. Decoupled and Standalone

Journeys are configured as regulator-compliant Progressive Web Apps hosted outside the main banking application. This places them outside the scope of app store reviews, release calendars, and code-freeze windows. A campaign such as “Convert ₹50,000 to EMI” can be configured and deployed within days, with no native app build required.

2. Instant Distribution Through High-Conversion Channels

The engine generates unique, customer-specific deep links and distributes them through the bank’s owned channels: WhatsApp, SMS, and email. The customer receives a personalized message, taps once, and lands inside a secure journey pre-populated with their context.

The platform supports the full transactional flow end-to-end, rather than only the message layer.

3. Smart and Targeted Through Tags and Nudges

Two layers drive targeting:

- Smart Tags are behavioral and demographic markers that identify the right customer cohort for a given journey.

- Smart Nudges are event-based triggers that initiate the right journey at the right moment — post-transaction, on threshold breach, or on inactivity.

A high-value customer with a recent ₹50,000 electronics spend can receive a WhatsApp nudge offering EMI conversion, while a near-limit customer receives a credit limit increase journey. Both are managed from the same platform.

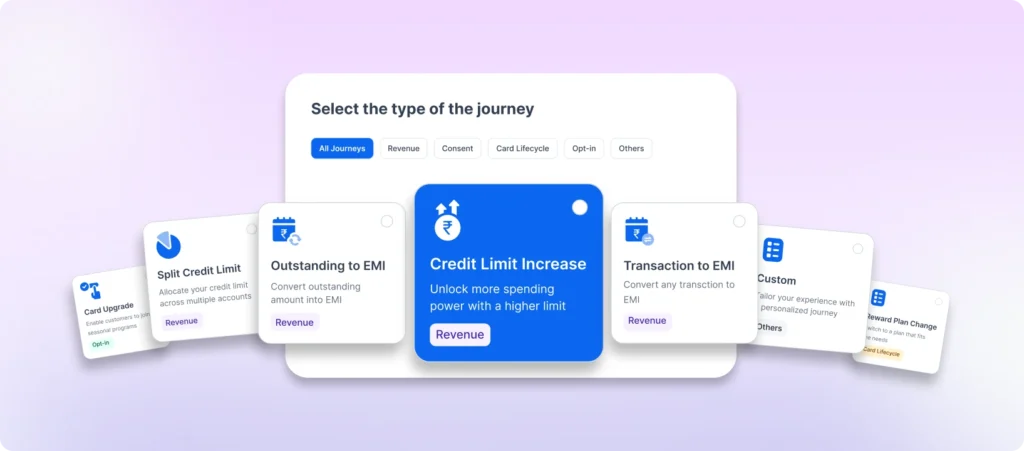

What Banks Can Launch with a Journey Builder

Hyperface Journey Engine ships with a pre-built library of lifecycle journeys configurable to the bank’s risk policy, branding, and segmentation logic. Here we discuss up-sell and cross-sell campaigns specifically.

| Journey Type | Use Case | Revenue Impact |

| Transaction to EMI | Convert specific transactions into easy EMIs | Direct interest income |

| Outstanding to EMI | Convert revolving balances into structured EMI plans | Reduces delinquency, boosts NII |

| Multi transaction-to-EMI | Convert multiple transactions at one go into EMI | Boosts interest income |

| Split Credit Limit | Allocate limits across multiple accounts or users | Customer retention |

| RBI Card Active Consent | Capture compliant active-card consent | Regulatory compliance + activation |

| Plan Change | Switch customers to better-fit card plans | Reduced churn |

Each journey is available out of the box and fully configurable.

The Business Impact: Speed, Agility, and Measurable ROI

A decoupled journey builder delivers four primary outcomes.

Faster launch cycles. Banks operating on traditional rails often see launch cycles extending into months. A journey orchestration layer compresses this into days, changing the pace at which a bank can respond to market shifts.

Real-time analytics for ongoing optimization. Each journey ships with a live dashboard covering funnel data, day-wise completion trends, conversion rates, and drop-off points. Issues can be identified and resolved within the same campaign cycle.

Faster GTM for new partnerships. Historically, each new co-brand partnership has required a fresh integration sprint. A one-time integration with composable journey workflows allows banks to onboard partners with minimal incremental engineering effort.

Personalization without engineering lift. Because journeys are configured rather than coded, growth and product teams can launch hyper-personalized offers without engineering tickets. Variant testing across customer segments becomes a marketing function rather than a tech project.

These outcomes are observable in deployment data. A leading Indian private sector bank running cross-sell journeys on Hyperface Journey Engine reports 11x month-on-month growth in EMI conversions — a result of channel-distributed delivery, behavioral targeting, and in-campaign optimisation working together.

By leaving legacy systems untouched and layering modern API and journey infrastructure on top, banks gain the agility of a digital-first competitor without the risk and cost of replacing core systems.

How to Evaluate a Journey Builder for Your Bank

When assessing a customer journey builder for banking, the following capabilities should be considered foundational:

- App-independent hosting — journeys function without requiring entry into the native app.

- Multi-channel distribution — WhatsApp, SMS, and email at minimum, with deep-link personalization.

- Pre-built journey library — EMI, credit limit, consent, plan change, and balance transfer flows available out of the box.

- No-code configuration — product and marketing teams can deploy without engineering involvement.

- Real-time analytics — funnel visibility at step and cohort level.

- Compliance built-in — RBI-aligned flows, audit trails, and consent capture.

- Smart targeting — behavioral tags and event-driven nudges, rather than undifferentiated blast campaigns.

- Bank-grade security — token-based access, encrypted journeys, and protected PII handling.

In Sum

The shift from app-coupled journeys to a decoupled journey builder is structural rather than cosmetic. It changes which functions inside the bank own the launch cycle for revenue generating campaigns, what kinds of experimentation are possible between releases, and how quickly a campaign can go from idea to live.