Achieving Top-of-Wallet Status in 2025: Trends Issuers Can’t Ignore

As the credit card market matures and competition intensifies, the real battleground for issuers has shifted from customer acquisition to wallet share. Becoming the primary, go-to card—or “top-of-wallet”—is where issuers unlock the most value, from transaction fees and interest (APR) to long-term customer stickiness.

In its May 2025 report, The Credit Economy: Top-of-Wallet Credit Cards, PYMNTS Intelligence, a leading global data and analytics platform, offers timely insights into what drives consumers to choose and favour one card over others.

The study uncovers how consumers choose—and consistently use—their primary credit card. While the data is U.S.-centric, the behavioral trends offer strong parallels for India and broader Asia, where credit adoption, digital payment ecosystems, and user expectations are evolving rapidly.

For issuers in these markets, the findings offer a useful roadmap for designing habit-forming, high-utility card experiences.

1. Primary Cards Capture the Majority of Spend

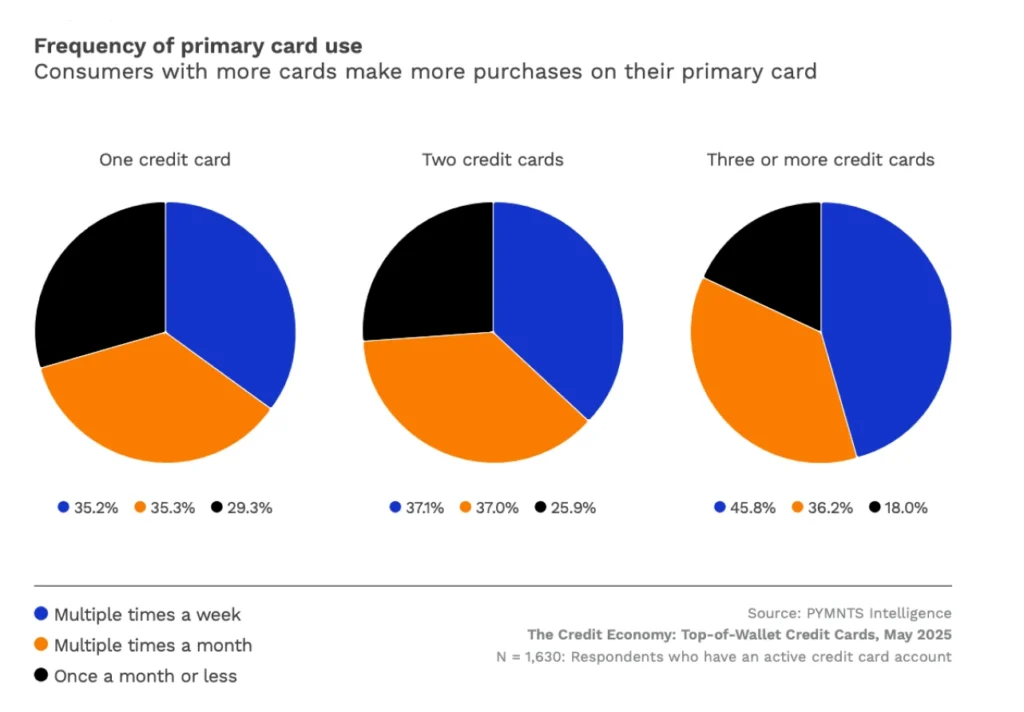

One of the report’s most counterintuitive insights: the more cards consumers own, the more likely they are to concentrate usage on a single one. Nearly half of credit cardholders (49%) have three or more cards, and among them, close to half (46%) use one primary card multiple times a week.

This card isn’t just used more—it carries significantly more value, with an average monthly balance of $1,900. That’s 58% higher than the second-most-used card ($1,200), and more than double the balance on the third-ranked card ($900). In other words, top-of-wallet cards can drive nearly double the revenue potential.

2. Rewards Remain the #1 Differentiator

Despite the rise of newer payment features and digital experiences, rewards continue to be the most influential factor in card selection. Nearly half of cardholders (48%) state rewards or discounts as a key reason for choosing their primary card, and 31% say it’s the single most important one.

The pull of rewards is even stronger among those who use their credit cards for everyday purchases—where frequency amplifies the impact of relevant, accessible rewards.

3. Younger Consumers Want Flexibility and Control

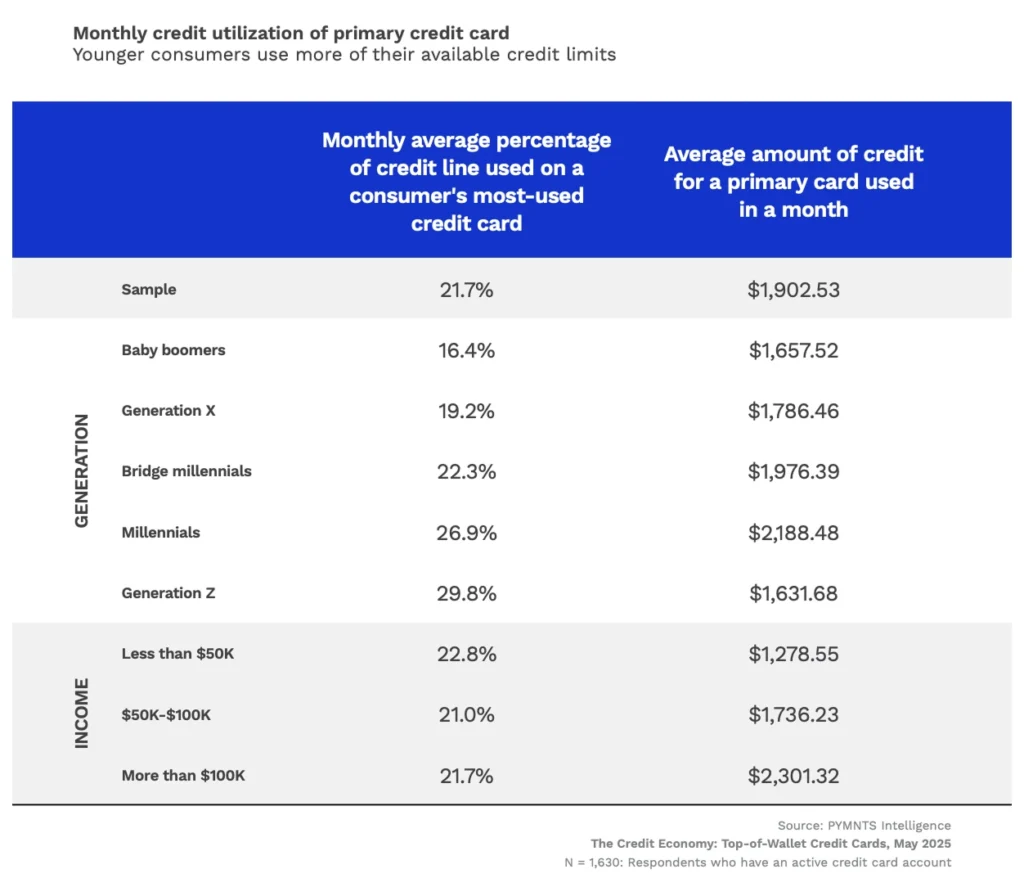

For Gen Z and millennials, access to credit is no longer enough. They expect control over how they use and repay it. Gen Zers use around 30% of their credit limit on average—nearly twice the share of baby boomers—and nearly half (48%) say they’d use their card more often if given the ability to choose payment modes at the time of purchase (installments, full repayment, or direct debit).

This generation also values spending insights, customizable limits, and the ability to pre-set payment rules—features that align with their app-driven expectations.

4. Usage Patterns Should Inform Product Design

How a card is used greatly influences what cardholders value:

- Everyday spenders prioritize rewards

- Bill payers and emergency users care about interest rate, credit limit, and card security

- Users with multiple cards are more likely to use their primary one for high-frequency, low-ticket purchases

This reinforces the need for context-aware product design, not just demographic segmentation.

What This Means for Issuers

For issuers, the shift is clear from focusing on card issuance and static features to building engaging, relevant, and flexible credit experiences.

Three Strategic Imperatives:

1. Design for Usage Context

Match your product features to the card’s intended use—whether that’s daily spend, emergencies, or lifestyle-based categories. A card built for everyday spending should offer relevant rewards and low-friction experiences. A card for emergency use may require strong security features or low-interest flexibility.

2. Embrace Payment Flexibility

Payment modes, spending insights, and personalized repayment options are no longer differentiators—they’re expectations, especially among younger users.

3. Focus on Driving Frequent Use

Top-of-wallet cards win through habit. Features like micro-rewards, dynamic nudges, unified loyalty systems, and seamless reward redemption create daily engagement loops.

Hyperface Smart Engage is a unified engagement platform for modern credit card portfolios. It helps issuers respond to these evolving expectations with:

- Dynamic customer cohorting at scale and personalized campaign triggers

- Real-time nudges and milestone gamification

- Multi-currency rewards ledger with configurable rules and expiries

- Seamless rewards redemption across multiple partners

- Real-time, actionable insights for customer lifecycle management

Built for the demands of today’s digital-first credit users, Smart Engage empowers issuers to act fast, stay relevant, and compete where it counts—on cardholder engagement.

👉 To learn more about Hyperface solutions, talk to our team.